Banking app: why would anyone need it?

In 20th century, you could have told if the bank was successful by looking at the size of the chandelier in their head office. Old historic building, a safe room full of gold and a lot of suits around. However, in the 21st century, bank office is a buzzing hive — waiting lines, annoyed managers, and endless paperwork. Nowadays we are used to having a small bank office close to our residence, but do we really need those anymore?

There are banks operating without any offices, for example, ING Direct, and other online banks. Most banks have websites where they process client requests, and now some are starting to have apps as well. We are getting used to instant money transfers from the screens of our smartphones. Let’s take apart banking mobile apps and see what they actually offer (or should offer) — simple convenience for the clients, or additional savings for the banks?

How modern banking works?

Every bank has two distinct directions in their client-oriented activities:

1. Acquiring clients for the banking products.

2. Operating existing clients according to their chosen products.

Traditional way of getting a client to buy banking products is through personal contact with manager in the office of the bank, and loads of paperwork. Following this scenario, online banks operate through a network of mobile managers that sign the clients up on the spot via specifically designed CRM systems. Most innovative banks are willing to make client choose and buy products themselves online, and there is no particular problems with this method. However, the focus of this article is on the second activity, namely, services provided to the existing clients.

Servicing existing clients, banks bear a number of costs that add up to form service expenses, mainly consisting of maintenance cost of request processing infrastructure. Obviously, any bank wants to reduce operating costs by redirecting the clients to the cheapest operating channels.

Nowadays, you can expect to have several bank operating channels, including:

— Orthodox, an in-person visit to the bank’s office. Operating costs include rent, wages, consumables, etc. Offices have issues related to capacity and location — no one will visit an office in the middle of the desert. Banks typically compensate for inability to have an office in every block by setting up ATMs for cash deposits and withdrawals. Some banks have mobile offices that drive through less populated areas to provide services.

— Phone call, another more traditional way of dealing with requests. After identification, client can request any operation through a call-center. Call-centers are a cheaper way of processing requests as those can be outsourced from lower wage regions.

— Online banking, a recent invention that became a very important operational activity platform. Clients go through two-factor authentication to get their requests processed, usually authorizing transaction from their password-protected profile via a confirmation code messaged to them. Bank managers confirm that today online banks are frequently used from desktop and mobile devices.

— Mobile app, a rising method of dealing with a growing wave of mobile traffic to the bank’s website. Many modern banks are considering development of a native mobile app to process client requests. The potential of this channel is as huge as it is untapped by the modern banks.

Banking app as marketing tool

Nevertheless, banking apps are currently on the last place among the ways to process client requests. Some banks consider it an additional paid service, scaring clients away from reducing bank’s operating expenses.

An easy-to-use banking app, however, can be a tremendously efficient tool of increasing loyalty among the younger generations and tech-savvy crowd of advanced consumers. Some modern banks bet on having a good and accessible app, and rightfully so.

Today’s trends are that clients pick a bank not by the key financial indicators, but by non-direct factors like are they happy with day-to-day service, or does the bank have a handy mobile app. Moreover, App Store and Google Play provide additional marketing power for the apps, and good app can generate clients for the bank by itself.

From an operating tool mobile app becomes a new communication channel for the clients, fast and cheap. It is important to remember that mobile app is always in the client’s phone, and it is vital that it only brings positive emotions when interacted with.

How to make a proper app?

Now that we know an app can be a powerful marketing tool, affecting loyalty and optimizing bank’s expanses, lets discuss how to create an app that will get to the tops of app stores and deep in the hearts of the users. There are always two ways of doing something:

Wrong: put in all the features, users will figure it out

The traditional, feature-focused approach of transferring all the functions of online banking to the app, is fundamentally wrong from usability standpoint. While developing an app, banks should consider their user’s problems first and foremost.

Right: solve your client’s problems

To properly feel the problems users face, take your barely charged smartphone with you on a rainy (better yet, snowy) day out and try to use some sophisticated app. Now ask yourself a question — which features user really needs?

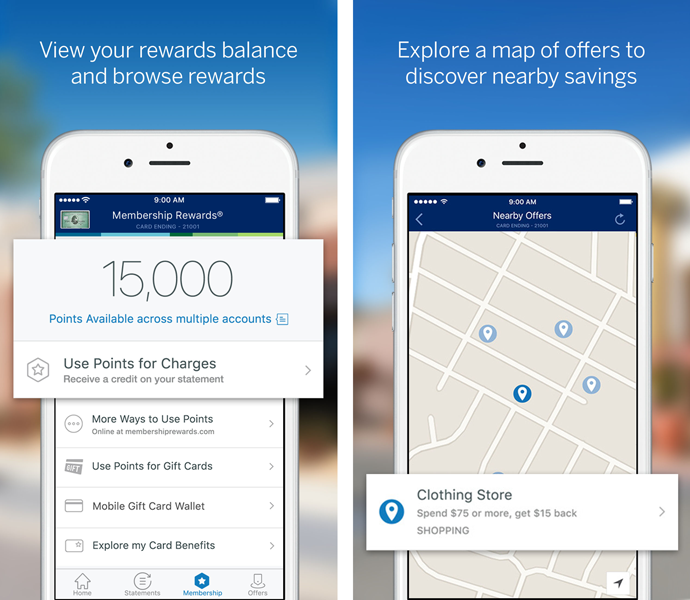

And here is an unexpected answer: user needs big control buttons with clear functions, so he can check his balance while holding several bags in the grocery. User needs simple money transfer templates to send funds to the regular recipients (spouse, kids, parents, etc). User needs a comprehensive spending report with breakdowns so they can control their budget — in fact, this feature may even stimulate some clients to open an account in your bank.

The solutions are endless: instant credits, insurance, transactions, payments, discounts, free VoIP calls from abroad. By keeping an open mind, bank can create an app with a myriad of features, useful and even valuable to the clients, skyrocketing app’s marketing potential.

Remote banking of XXI century — new frontiers

The question is in the air for the bank management during optimization meetings: will banks shift from old dusty offices to the dispersed online service providers?

It is clear today that the future is in synergy — banks change from a place you go to get a mortgage to a sort of invisible companion that helps you manage your finance on a daily basis. Today it loans you a holyday money, tomorrow sells you an insurance for it, and gives a discount coupon the day after.

From the interest-generating piggy bank, modern banks transform to an operator, that is not only works with personal or corporate finance, but also sells traffic to its partners. Some banking apps offer great deals based on location, or even user interest.

Always remember that users who install an app provide valuable statistical data, unique to the nature of smartphone apps. If a bank can use this data to increase loyalty and reduce operating costs, it can extract great value from app and help acquire more long-term clients.